Decades of Experience,

Dedicated to You

Dedicated to You

Chapter 7 bankruptcy is a process to have the debt discharged while maintaining your home and other assets by taking advantage of California bankruptcy exemptions. Because the bankruptcy court conducts all meetings on Zoom, you will not have to appear in person. There is no minimum amount of debt required to file Chapter 7 bankruptcy. Your bankruptcy lawyer will determine if you are eligible for Chapter 7 using your median income and the means test.

Almost all Chapter 7 bankruptcy cases are No-asset cases, which means you don’t have anything to give back to a creditor that doesn’t fall under the California list of exemptions. Debtors will not lose typical personal property ordinarily found in homes during Chapter 7, but all property must be on your bankruptcy petition.

Your bankruptcy attorney will help you choose between the 703 vs 704 exemptions when filing for Chapter 7 bankruptcy in California. Debtors with equity in their primary residence will typically use the 704 exemptions, including the Homestead Exemption, enabling them to keep their home in most cases. Debtors who do not own a home can use a wildcard exemption of up to $33,650 to exempt anything they want that is not already exempt under another category. You can keep $33,650 in cash while filing Chapter 7 bankruptcy if you do not have any other property you want to protect and use the 703.140(b)(5) wildcard exemption.

All financial assets must be declared when you file bankruptcy. The debtor must declare an asset before they can use the corresponding exemption for it. You must provide all financial documents when filing bankruptcy, regardless of whether they are joint or single accounts. After you provide all account statements, the bankruptcy trustee will not continue to monitor your accounts unless you fail to disclose any assets.

A widespread reason people file bankruptcy is when they start small businesses and face financial challenges. The company can file for Chapter 7, known as “liquidation” bankruptcy, because the trustee will liquidate all the business assets.

Debtors with ownership stake in a company can still file for Chapter 7. The value of the business will directly affect the debtor’s ability to pass the means test. If the debtor owns a small business, certain assets like tools, computers, phone systems, desks, and chairs can be exempt using the “tools of the trade” exemption. If the debtor can still pass the means test without liquidating the business, they can continue operations normally during bankruptcy.

No minimum or maximum debt is required to file for Chapter 7 in California. If you pass the means test and are below the California median income, you qualify for Chapter 7 and get a fresh start.

When you file for bankruptcy, you address three types of debt: secured, unsecured, and priority. Secured debt means a physical asset the creditor can repossess exists to secure the debt. Houses, vehicles, boats, and even the shed in your backyard are examples of secured debt. Unsecured debts are typically discharged in a Chapter 7 bankruptcy because there is nothing to give back to the creditor. Priority debt tends to be IRS or other debts the federal bankruptcy court gives “priority” and usually cannot be discharged.

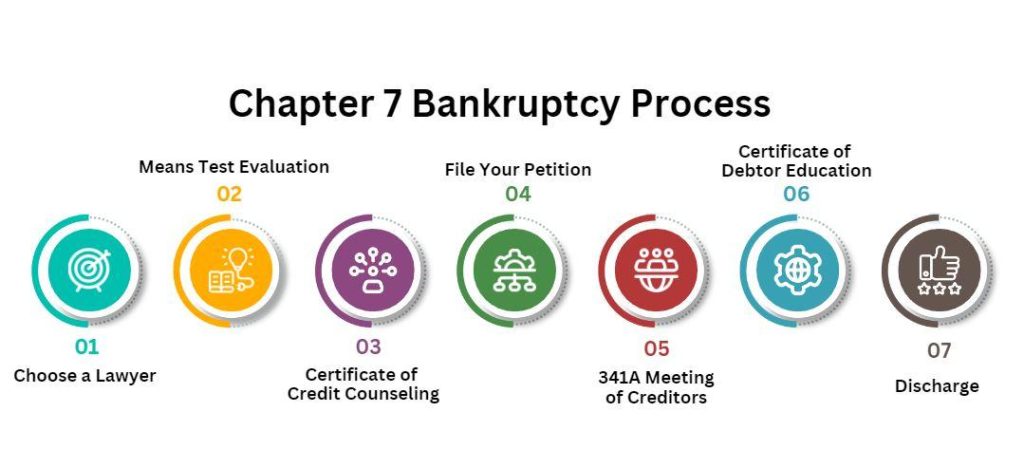

After you file your bankruptcy petition and pay the filing fee, it will take about a month until your 341A hearing. The California Chapter 7 Bankruptcy process takes about three to four months. However, your case can take longer (up to six months) if there are additional questions after your 341A hearing.

To file for Chapter 7 in California will cost between $1,500 – $2,500, including the filing fee to have a lawyer represent you throughout the California bankruptcy process. In 2024, anything outside this range is either too cheap for you to get the adequate attention your bankruptcy deserves or too expensive.

Everyone worries about their credit score when they file for bankruptcy. You will likely lose points with a high score of 700-800. However, you will likely gain points with a lower score from 400-500. You will lose all your credit card accounts even if you have religiously made monthly payments. A bankruptcy case will appear on your credit report as a public record for up to 10 years, making securing business or personal loans more challenging.

Your lawyer will do a complex analysis to determine if you can pass the Chapter 7 bankruptcy means test. The means test ensures only debtors who cannot pay back the debts they owe in a reasonable time frame could file for Chapter 7. Otherwise, the debtor must pay back at least part of the debt through a Chapter 13 bankruptcy over 3-5 years. To pass the means test, the debtor must not have significant disposable income and must be under the median income in California for a household of the same size. Your bankruptcy attorney will use your paycheck stubs to determine if you are under the median income in California and qualify for Chapter 7.

If you are married, you should discuss your options with an attorney. When doing a single filing, your partner’s credit will remain unchanged, making it easier for you both to use their credit while building up your post-bankruptcy credit. Couples also have flexibility in deciding whether a dual salary makes more sense or if just one of the people in the couple should file. Because federal law does not recognize gay marriage, there is even more flexibility, and those couples can decide what is best for them by calculating whether being a couple is financially beneficial regarding their bankruptcy case.

It is not unheard of for people to file for Chapter 7 by themselves, which is called “pro se.” However, we do not recommend doing this as it can be a complicated process with many nuances. Even those who manage to get it done without paying for an attorney may have missed an ample opportunity on exemptions or inadvertently gotten their bankruptcy case dismissed because they missed crucial parts of the process or deadlines. If you want to move fast and impress your lawyer with how prepared you are, the following requirements are essential in California bankruptcy.

Please note there may be more documents required depending on your situation.

Finding a good lawyer that makes you comfortable is significant, and there are a lot of lawyers in Riverside County. I would recommend talking on the phone to at least 2-3 lawyers, and if they are “too busy” to give you the initial consultation to get to know one another, move on to another lawyer. Be sure to find a lawyer you connect with and feel comfortable with, both in how they talk to you and in their knowledge of the details of your case. Your lawyer, preferably, is well-versed in California law and has filed thousands of bankruptcies in the Central District. You have to be completely honest with your lawyer as they work for your rights, not for the bill collectors or the court. You may be surprised how often people feel embarrassed about their situation and lie to their lawyers, putting themselves in a precarious situation.

Now, you can meet with your attorney and explain your exact situation regarding your income, property, debts, expenses, spousal support situation, and urgency. Your lawyer should ask many questions about your life, in general, to understand where you are financially and what the best path forward is for you under the law. Your lawyer will pull your credit report, giving you a list of creditors in all three credit reporting bureaus. Your lawyer will add all your creditors to your bankruptcy petition. During this meeting, your lawyer will compare your salary to the median income to determine if you qualify for Chapter 7.

The bankruptcy court wants to be sure that debtors learn about money management during the process. You are required to take the first credit counseling class to understand the basics of money management, budgeting, and responsibly using credit. You must include your attorney’s code so the system automatically credits you for taking the class.

When I file your Chapter 7 bankruptcy petition with the court and the pay the filing fees, you immediately get an automatic stay by the court. Most bankruptcy attorneys file petitions in batches because if they have ten clients filing, all the court dates will line up, making it easier for everyone. However, I will make an exception if you have an urgent situation like a foreclosure or repossession.

Now that you have filed bankruptcy in California, the Federal court will issue you several things:

The 341 Meeting of Creditors is your first meeting with the court; attendance is mandatory for all debtors and their attorney.

A trustee represents the court and works in the creditors’ best interest. Their job is to ensure you are not taking advantage of the system, and if there is something they can sell to pay the creditors, it is their job. The trustee will also check your schedules carefully and ensure no signs of fraud. An experienced attorney knows all the trustees and judges in the Central District of California and can help predict differences in how they will conduct the process. Each district has A limited number of trustees, and an experienced attorney in your region will know them all quite well.

From filing your bankruptcy petition until discharge will last about 3-4 months, and during that time, you must:

If you are paying a mortgage, you cannot access online accounts. You must pay by mail or phone, and your bank can help advise you on how to keep making mortgage payments. If all goes well about 60 days after your 341A Meeting, the trustee will declare your case a no-asset case, and all your unsecured debts will be discharged.

The Certificate of Debtor Education, required for Chapter 7 bankruptcy filers, must be completed post-filing but pre-discharge. This approximately two-hour course can be taken at home using an online tool, in-person, or by phone and covers financial literacy topics such as budgeting, money management, wise credit use, and financial planning. The filing fees do not cover The certificate of debtor education class and the credit counseling course. A certificate must be issued and filed with the bankruptcy court upon completion. The course filing validates all debtors took the course.

To receive a Chapter 7 discharge in California, you must first qualify through a means test demonstrating that your income is below the state median or you lack sufficient disposable income. Complete both credit courses and submit all required documents, including the bankruptcy petition and financial schedules. Attend a 341 meeting with creditors where the trustee oversees discussions about your financial situation. Post-filing, complete a mandatory financial management course. The trustee will review assets and liabilities, and if creditors raise no objections within 60 days post-341 meeting, the court will likely issue a discharge.

Surrender, Reaffirm, Retain, and Pay After filing for bankruptcy, The debtor must determine how to handle their secured debt. Chapter 7 bankruptcy has three options: Surrender, Reaffirm, or Retain and Pay. A vehicle would be an excellent example of a secured debt going through this process. If the debtor decides they do not want the car anymore, they may halt payments and Surrender the vehicle to the creditor, and the debt will be discharged during the bankruptcy process. The debtor may also sign a Reaffirmation Agreement with the creditor, removing the secured debt from the bankruptcy. It is important to note that a Reaffirmation Agreement is outside the bankruptcy, and the debtor must have sufficient income and will be responsible for the repayment plan. The bankruptcy can no longer discharge the debt after the debtor has agreed to reaffirm the property. If the debtor decides to Retain and Pay, the debtor retains the collateral and does not sign a Reaffirmation agreement. The property will remain in the debtor’s possession if the debtor stays current on the payments. The debtor will receive the title or gain full ownership of the collateral once it is paid in full. If the debtor has late payments or defaults during Retain and Pay, the creditor will immediately repossess the asset without warning.

There are many bankruptcy attorneys in the Central District of California, but only some excel. I can help you protect your property with either Chapter 7 or Chapter 13 bankruptcy. With offices in Riverside, San Clemente, and Palm Desert, I can offer my services throughout most of Southern California. I speak fluent Spanish, answer the phone personally as much as possible, and will file your bankruptcy as quickly as possible if urgency is required. Contact me today for a free consultation.